The capacity meets the structural limits to the second quarter of 2026.

At a glance, Spain enters the second half of this year as one of Europe's most efficient economies, which is most evident in the pace of tourist activity in all its major cities. Last year, Spain welcomed 96.8 million visitors: the highest number ever. In the first two months of 2026, approximately 10.7 million people visited the country, which is a 2% year-on-year increase.

The GDP numbers confirm the view. After GDP growth of 2.8% in 2025, the Bank of Spain recently increased its forecast for 2026 to 2.3% from 2.2%. At the same time, it has warned that energy-related shocks could lead to its basic charge slipping away. With or without volatility in the Middle East, the central bank sees 2027 GDP growth of 1.7%, down from its December forecast of 1.9%.

By comparison, most estimates for 2026 predict that the eurozone will grow between 1.1% and 1.3%, while major economies such as Germany and Italy are expected to lag behind.

The comparative strength in Spain however sits next to the growing structural inequality, such as the housing shortage and the energy benefits obtained from the evolution of the energy mix, both of which will help to determine whether growth translates into strong financial stability or begins to force it.

Banking: Power or Position?

An important question for investors and businesses is whether the Spanish financial system will improve to support growth.

The collapse of Banco BBVA's bid for Banco de Sabadell last fall removed what had been the most obvious form of equity in Spain's banking sector. What will replace it is not clear.

On the surface, Spanish banks look very strong. Profitability remains among the highest in Europe, capital levels are strong, and banks continue to reward shareholders with dividends and buybacks. BBVA's €3.96 billion plan is just one example of a broader trend across the sector, which also includes Banco Santander, which says it will return at least €10 billion to shareholders between 2025 and the end of this year.

However, Santander is combining capital gains and expansion with its pending merger of Webster Bank in the US, the ongoing development of its digital platform Openbank—now active across Germany, Portugal, the Netherlands, the US, and Mexico—and its broader One Transformation strategy aimed at creating a more unified global platform.

Not all banks have a large enough capital base to pursue both a popular reverse plan and a global, digital-first expansion strategy. That points to a problem facing all Spanish banks. Without further consolidation or a reasonable push to expand borders, parts of the sector may remain highly efficient domestically but are limited in scale compared to the larger European cross-border banking groups.

“There is still room for consolidation in the system,” said Ángela Cruz, executive director, Ratings of Financial Institutions in Scope Ratings, noting that the strong organic growth and proprietary structures may reduce incentives for additional agreements. “Spanish banks are not at a disadvantage in this respect.”

The issue, in other words, is not immediate weakness; whether today's forces are reducing the urgency to pursue scale while conditions are still favorable. Going into the second half of 2026, the problem is less about profitability – which remains strong – and more about the trajectory. Are Spanish banks improving what they already have, or positioning themselves for what's next?

Housing Issues

That question is starting to play out in the housing market. Unlike the global credit collapse of 2008, today's risk is not a bank default, but a structural imbalance between supply and demand and how that imbalance is changing the mortgage market.

Spain is not facing a demand crisis. “Looking ahead to H2, we expect mortgage growth to remain driven by supply shortages rather than demand or credit conditions,” said Pedro Álvarez Ondina, economist at CaixaBank Research.

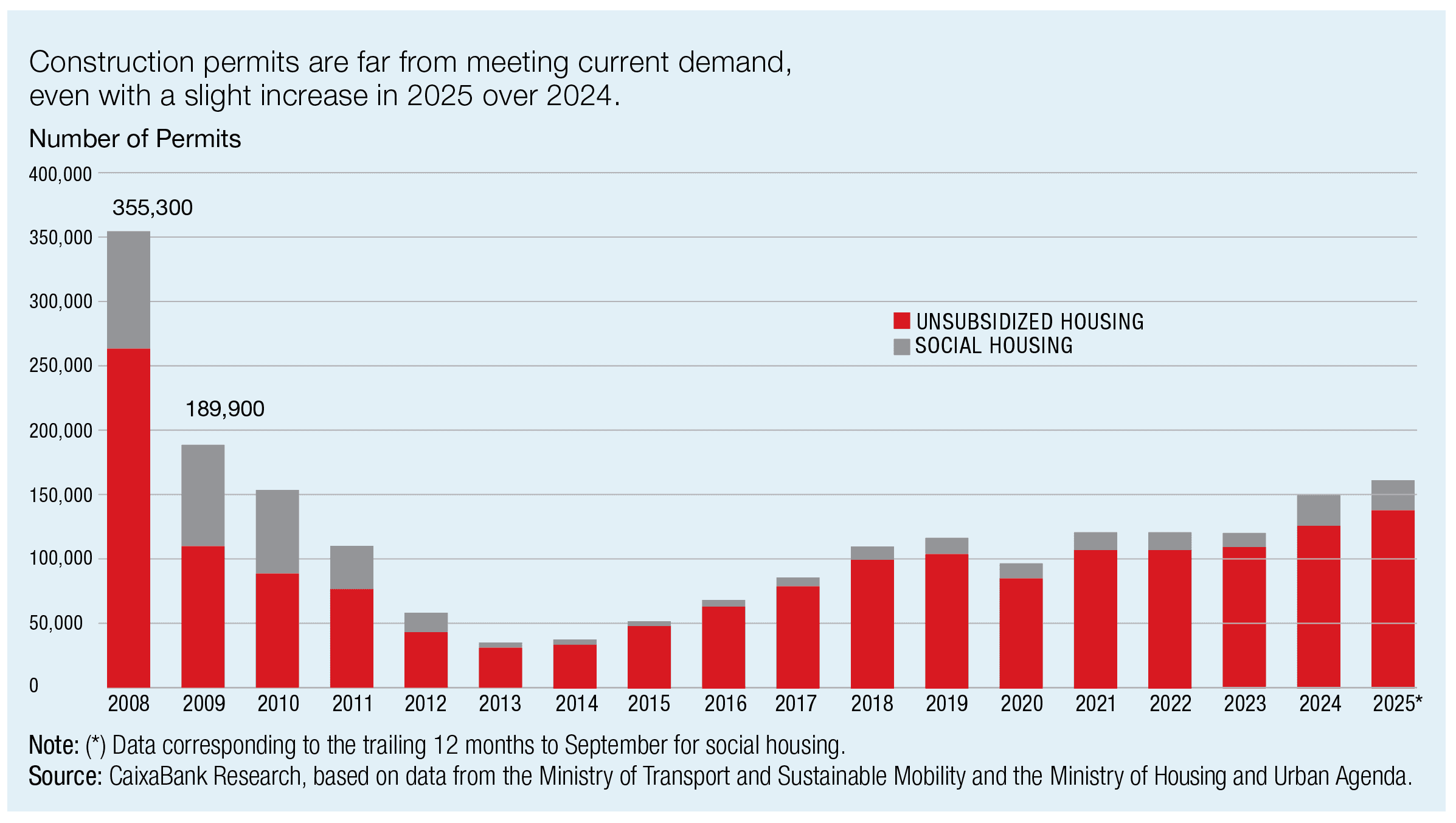

Despite a supply shortage that has grown to more than 730,000 homes as of 2021, new building permits fell by nearly 54% from 355,300 in 2008 to just 162,195 last year, according to CaixaBank Research. The imbalance continues to support prices, especially in sought-after areas such as Madrid, Barcelona, Valencia, Alicante, and Málaga. From the banks' point of view, it also strengthens asset quality by limiting the risk of sharp corrections.

“Limited supply helps reduce price risk,” notes Álvarez Ondina, “but it is increasingly acting as a drag on the growth of mortgage rates.”

Scope's view is broadly consistent with that analysis, but flags some additional pressure points. “Home price growth is outpacing disposable income,” Cruz says. [loan-to-value] mortgage lending has increased. But there is no indication of imminent asset quality pressure.”

The demand structure is also changing.

“The decrease in the share of home purchases without a mortgage – from about 35% to 30% – should not be interpreted primarily as a cooling of foreign or wealthy buyers,” said Álvarez Ondina. “Instead, it shows a normalization of financial conditions after the major tightening of 2022-23.” With the cost of borrowing stable, profitability has become attractive again, even for consumers with the ability to pay with cash.

For banks, this presents a very different second half outlook.

Rising collateral values and an undersupplied structural market continue to support credit quality. The pace of new lending is increasingly linked to housing supply and basic demand.

The bottom line is that the Spanish housing market shows no signs of weakening. Rather, it is restricted to supply in a way that continues to explain both price movements and the trajectory of credit growth.

Power as profit

If housing must be one possible financial obstacle to Spain's growth, the energy sector shows one of its clearest structural advantages.

The energy shock caused by instability in the Middle East has seen Spain less exposed to gas-driven electricity prices than many of its European peers. Thanks to the ongoing transition to renewables such as wind and solar, gas only contributed to the country's electricity price by 15% this year through early March, compared to 89% in Italy and 40% in Germany, according to Ember, a global energy think tank based in London.

Spanish brands have shown remarkable resilience in this area.

“Firms are now better prepared structurally,” said Álvarez Ondina, citing lower energy intensity, greater use of long-term contracts, and increased investment in productivity and efficiency. Going forward, he expects that these factors “should help reduce, although not completely eliminate, the shock to the price of renewable energy.”

But the system faces its own problems. As the penetration of renewables increases, price volatility becomes more difficult, with periods of overproduction pushing prices lower during peak production hours. This phenomenon, known as price cannibalization, sits alongside grid problems as a reason investors will be watching closely to assess how much capacity can be absorbed by the market before long-term yields come under pressure.

That said, the combination of a healthy tourism economy, a growing population, a strong housing market, and an energy advantage continues to make Spain an outlier in Europe's underperforming economies. Its next phase of growth will depend on the system's ability to support and grow them.

This article appears in the June 2026 issue of Global Finance Magazine.